Standard Deviation Measurement ToolIf you like the script please come back and leave me a comment or find me on the interwebs. I get notified you "liked" it... but I have no idea if you actually use it. So, let me know =)

The script uses the open price as the mean and calculates the standard deviation from the open price on a per candle basis

- Goal: -

To establish a mean based on the Open Price and calculate the standard deviation.

The reason for this is if the Open is the mean, then the Standard deviation implies a standardized distance a given candle can be expected to travel

from the open price

- Edge: -

If you know that there is a 68%/95%/99.7% probability that price will NOT move more than

One Standard Deviation/Two Standard Deviations/Three Standard Deviations from the open price respectively

you can set reasonable price targets that relate to those probabilities in a given timeframe.

e.g. if you're on a 1h chart and your target is 3.5% from the open price, but 1 standard deviation of the hourly candle is equal to 0.78%.

You can make assumptions on either:

- The reasonableness of your target

or

- The holding period likely required for the trade.

Also, Standard Deviation is a function of volatility and this tool provides a unique mechanism for measuring volatility as well on a candle by candle basis

- Customization Options-

- Set 3 independent upper and lower standard deviations.

- Each set of standard deviations are on a switch so you can show 1, 2, or 3 sets of standard deviations

- You can set the distribution width

- Though it's not recommended, you can change the mean source.

- There is a switch to show the standard deviation on only the real-time bar or real-time and historical bars.

- How I Think About This Script -

This strategy is predicated the same principle as Bollinger Bands: the reality that 68% of all data points will fall within one standard deviation of the mean, 96% of all data points will fall within two standard deviations, and 98% of al data points will fall within 3 standard deviations. By understanding the standard deviation, you can possibly infer an edge by understanding the probabilistic range price will be bound to the limits of standard deviation rules according to their probabilistic outcomes for the single candle on any given timeframe. Bollinger Bands are designed to provide this information with the mean being a 20-period moving average and this indicator.

This indicator is designed to provide standard deviation information with the mean being based on the distance price travels away from the open of individual candles in the lookback period.

If you use a strategy where you enter on major candle closes, this can be useful to set targets for those entries based on the intended hold period or at least add/remove validity to other target metrics.

Example:

Your target is at the 1.618 Fibonacci level and your confirmation triggers on the 4h candle close (H4 if that's your thing lol). You set up the indicator based on the standard deviation of price movement in 4h candles over the last week.

Let's say the indicator shows that the 1.618 Fibonacci level is 3 standard deviations away.

This being the case this statistically indicates that within the next 4 hours, you have a very low probability of achieving your target (>2%). This doesn't invalidate your target, but it does indicate a low probability of achieving it in the next 4hrs. With this information, you can infer that you are either going to be (a) really lucky (b) in this trade for a lot longer than 4hrs or (c) your target is unrealistic given your intended hold period.

You can develop a more probabilistically favorable hold period calculation by looking at the standard deviation on a higher time frame (e.g. 1d-1w).

Bonus feature: You'll find that the 2 and 3 standard deviations will often "cluster" and these clusters often provide future S/R levels. That's a pretty sweet feature no one things to look for. But, try it. Find a cluster of 2nd and 3rd stdevs that are in somewhat of a horizontal pattern (usually the result of a range) and you'll find that to be a good s/r area. Even better if you use the 3.2 standard deviation, you'll find that is a fantastic breakout signal!

Summary

So, you can use it for target setting, a confluence test, a reasonableness test, or just a measurement tool.

This was the first TV script I ever wrong.. Got taken down. But, I've re-released it because there are other TV scripts that attempt to do this but are completely wrong.

Please be careful about using other people's scripts. Always validate the math of the script before you use it if possible.

Stay safe out there and I hope all your dreams come true.

Wyszukaj w skryptach "THE SCRIPT"

Accumulation/Distribution Open Interest Money Flow Hi, this script is the version of Accumulation / Distribution Money Flow (ADMF) that uses Open Interes ts in the required markets instead of Volume.

Can be set from the menu. (Futures/Others)

NOTE: I only modified this script.

The original script belongs to cl8DH.

Original of the script:

I think it will make a difference in the future and commodity markets.

Since the system uses CFTC data, use only for 1W timeframe.

With my best regards..

BACKTEST SCRIPT 0.999 ALPHATRADINGVIEW BACKTEST SCRIPT by Lionshare (c) 2015

THS IS A REAL ALTERNATIVE FOR LONG AWAITED TV NATIVE BACKTEST ENGINE.

READY FOR USE JUST RIGHT NOW.

For user provided trading strategy, executes the trades on pricedata history and continues to make it over live datafeed.

Calculates and (plots on premise) the next performance statistics:

profit - i.e. gross profit/loss.

profit_max - maximum value of gross profit/loss.

profit_per_trade - each trade's profit/loss.

profit_per_stop_trade - profit/loss per "stop order" trade.

profit_stop - gross profit/loss caused by stop orders.

profit_stop_p - percentage of "stop orders" profit/loss in gross profit/loss.

security_if_bought_back - size of security portfolio if bought back.

trades_count_conseq_profit - consecutive gain from profitable series.

trades_count_conseq_profit_max - maxmimum gain from consecutive profitable series achieved.

trades_count_conseq_loss - same as for profit, but for loss.

trades_count_conseq_loss_max - same as for profit, but for loss.

trades_count_conseq_won - number of trades, that were won consecutively.

trades_count_conseq_won_max - maximum number of trades, won consecutively.

trades_count_conseq_lost - same as for won trades, but for lost.

trades_count_conseq_lost_max - same as for won trades, but for lost.

drawdown - difference between local equity highs and lows.

profit_factor - profit-t-loss ratio.

profit_factor_r - profit(without biggest winning trade)-to-loss ratio.

recovery_factor - equity-to-drawdown ratio.

expected_value - median gain value of all wins and loss.

zscore - shows how much your seriality of consecutive wins/loss diverges from the one of normal distributed process. valued in sigmas. zscore of +3 or -3 sigmas means nonrandom realitonship of wins series-to-loss series.

confidence_limit - the limit of confidence in zscore result. values under 0.95 are considered inconclusive.

sharpe - sharpe ratio - shows the level of strategy stability. basically it is how the profit/loss is deviated around the expected value.

sortino - the same as sharpe, but is calculated over the negative gains.

k - Kelly criterion value, means the percentage of your portfolio, you can trade the scripted strategy for optimal risk management.

k_margin - Kelly criterion recalculated to be meant as optimal margin value.

DISCLAIMER :

The SCRIPT is in ALPHA stage. So there could be some hidden bugs.

Though the basic functionality seems to work fine.

Initial documentation is not detailed. There could be english grammar mistakes also.

NOW Working hard on optimizing the script. Seems, some heavier strategies (especially those using the multiple SECURITY functions) call TV processing power limitation errors.

Docs are here:

docs.google.com

KK_Intraday MAsHey guys,

today I was browsing through intraday Charts looking at some moving averages. Basically what I wanted to see was whether the currency pair was trading below or above the moving average of the day/week/month. For a better understanding: The daily MA on a 15 minute Forex Chart would be the 96 MA.

I encountered the problem that i always had to change the settings for my MAs when changing the Time Interval, so I coded this here up. It is pretty simple but maybe somebody else has the same problem and can put it to use.

The script has some settings as listed below:

Choice which MAs to plot, (Daily, Weekly, Monthly)

Choice which type of MA to use (Simple, Exponential, Weighted)

Neccesary Settings for the correct calculation (e.g. Number of trading hours per day). These settings depend on the instrument you are using and should always be checked before using this script.

There are a few things to Note when using this script:

This script works for intraday charts only.

The monthly MA doesn't work on any Time Interval smaller than 15 minutes. Can't do anything about it unfortunately.

This is my first published Script, use it with caution and let me know what you think about it!

Moon Phases Final Moon Phases Visualizer DescriptionThis script is a comprehensive tool for traders who incorporate lunar cycles into their analysis. Unlike many basic indicators, this one is optimized for Pine Script v6 and utilizes a precise astronomical calculation based on the synodic month cycle ($29.53059$ days).The indicator helps identify potential "turn window" periods often associated with New Moons and Full Moons in financial astrology and cyclical analysis.Key FeaturesDual Visualization: Displays a smooth lunar cycle oscillator ($0-100\%$) in a separate pane while simultaneously plotting phase labels directly on the price chart.Smart Overlays: Using the latest force_overlay technology, the script keeps your price scale clean while showing Moon emojis (🌕/🌑) and an info table in the main area.Real-time Tracking: An elegant dashboard in the top-right corner shows the current phase percentage and status at a glance.Full Moon & New Moon Alerts: Visual signals are generated at the exact peak of the cycle, making it easy to spot historical correlations with price reversals or volatility spikes.How to read it:🌕 Full Moon (50%): Often associated with high volatility or local price extremes.🌑 New Moon (0%/100%): Often marks the beginning of a new cycle or a potential trend exhaustion.The Curve: Watch the oscillator to anticipate approaching lunar events before they happen.Technical DetailsThe calculation is anchored to a high-precision historical New Moon timestamp (January 6, 2000), ensuring the phase accuracy remains consistent even when scrolling back through years of historical data.

Disclaimer: This indicator is for educational and entertainment purposes only. Lunar cycles are a part of financial astrology and cyclical analysis, but they should not be used as a standalone signal for trading. Past performance does not guarantee future results. Always use proper risk management and combine this tool with other technical or fundamental analysis methods. Not financial advice.

Bear & Bull Builder // visual strategy builderAre you a trend follower?

Trend following systems have been a cornerstone of trading since the first candlestick charts were invented in 18th-century Japan by Munehisa Homma (or Honma), a legendary rice merchant who used them to analyze market sentiment and predict price movements. Since then, legendary traders like Richard Dennis and Dr. David Paul have used technical analysis—the study of turning points and trends of candlestick charts—to develop an edge and strategy for trading equity, commodity, and forex markets.

How to Utilize the Bear & Bull Builder

This script is a way to pick and choose technical methods like SMAs and EMAs to define trend exits and entries. Additionally, you can specify an ATR (Average True Range) calculated stop loss based on your individual strategy and trading plan. Within the settings panel, you can set up this script to display only Long Position values, zones, and levels—or configure it for shorts, or both.

What Makes This Original

Unlike most trend-following indicators that lock you into a single approach, this script lets you combine different indicator types (RSI, WaveTrend, CCI, EMA, SMA) across three separate trend timeframes. The originality comes from the flexibility: you can test whether momentum-based trends (like RSI) work better than moving averages for your timeframe, or experiment with mixing them together. The script also bridges the gap between manual trading and automation by providing visual position values and fill zones that show exactly where signals generate versus where orders execute—critical information most scripts ignore.

Getting Started

For this quick and easy setup example, I built a strategy that is long-only, displays only long positional data and values, and uses a 21 & 55 period exponential moving average for the short and medium-term trend in addition to an 89 period simple moving average for my longer-term outlook. I have set my ATR-based multiplier to 0.75, and have left the fill zone display turned on to help visualize when to set up the built-in alerts for automating my strategy. I have made this the default settings of the script.

Positional Values

GREEN NUMBERS → Entry signal price

YELLOW NUMBERS → Stop loss price

BLUE NUMBERS → Exit signal price

IMPORTANT

I cannot describe how useful it is to use TradingView's built-in Long and Short position tools! The whole reason for this script is that it is as manually friendly as it is automated—especially for backtesting. You can use the long position tool to measure exact profits and losses on individual trades for the strategies you build. This can really help you see clearly if you have built a system with positive expectancy.

Tables

1. Settings Display Table

Displays the trend types that are configurable in the settings panel. Shows if positional values for longs and shorts are currently displayed.

2. Back testing Table

Displays the total amount of long and short entry signals since the first bar of the chart. Additionally, it displays the average amount of bars per trade (time in trade).

Alerts & Automation

There are 4 built-in alerts for automating your strategy to an external server:

1.Long Entries

2.Long Exits

3.Short Entries

4.Short Exits

Since this script uses confirmed bar states for alert generation (to avoid repainting), all alerts and displayed position values (the green, yellow, and blue numbers) will be sent on the closing price. Each alert has a placeholder preset for further customization.

Technical Details

How the trend detection works:

Bullish state triggers when close > all three selected trends

Bearish state triggers when close < all three selected trends

Uses barstate.isconfirmed to prevent repainting

Stop loss calculation:

Long stops: highest_trend - (ATR × multiplier)

Short stops: lowest_trend + (ATR × multiplier)

ATR period is fixed at 20 bars, multiplier is user-adjustable

Entry placement logic:

Long entries execute at the highest value among the three selected trends

Short entries execute at the lowest value among the three selected trends

This ensures entries occur near the support/resistance created by the trend lines

Why calculate all indicators upfront:

The script calculates all five indicator types (EMA, SMA, RSI, CCI, WaveTrend) for all three trend lengths on every bar, then selectively uses the ones you choose in settings. This prevents Pine Script consistency warnings while maintaining flexibility.

Stock Relative Strength Rotation Graph🔄 Visualizing Market Rotation & Momentum (Stock RSRG)

This tool visualizes the sector rotation of your watchlist on a single graph. Instead of checking 40 different charts, you can see the entire market cycle in one view. It plots Relative Strength (Trend) vs. Momentum (Velocity) to identify which assets are leading the market and which are lagging.

📜 Credits & Disclaimer

Original Code: Adapted from the open-source " Relative Strength Scatter Plot " by LuxAlgo.

Trademark: This tool is inspired by Relative Rotation Graphs®. Relative Rotation Graphs® is a registered trademark of JOOS Holdings B.V. This script is neither endorsed, nor sponsored, nor affiliated with them.

📊 How It Works (The Math)

The script calculates two metrics for every symbol against a benchmark (Default: SPX):

X-Axis (RS-Ratio): Is the trend stronger than the benchmark? (>100 = Yes)

Y-Axis (RS-Momentum): Is the trend accelerating? (>100 = Yes)

🧩 The 4 Market Quadrants

🟩 Leading (Top-Right): Strong Trend + Accelerating. (Best for holding).

🟦 Improving (Top-Left): Weak Trend + Accelerating. (Best for entries).

⬜ Weakening (Bottom-Right): Strong Trend + Decelerating. (Watch for exits).

🟥 Lagging (Bottom-Left): Weak Trend + Decelerating. (Avoid).

✨ Significant Improvements

This open-source version adds unique features not found in standard rotation scripts:

📝 Quick-Input Engine: Paste up to 40 symbols as a single comma-separated list (e.g., NVDA, AMD, TSLA). No more individual input boxes.

🎯 Quadrant Filtering: You can now hide specific quadrants (like "Lagging") to clear the noise and focus only on actionable setups.

🐛 Trajectory Trails: Visualizes the historical path of the rotation so you can see the direction of momentum.

🛠️ How to Use

Paste Watchlist: Go to settings and paste your symbols (e.g., US Sectors: XLK, XLF, XLE...).

Find Entries: Look for tails moving from Improving ➔ Leading.

Find Exits: Be cautious when tails move from Leading ➔ Weakening.

Zoom: Use the "Scatter Plot Resolution" setting to zoom in or out if dots are bunched up.

Tristan's Devil Mark (Short / Long, with W%R)The Devil’s Mark indicator is a visual tool designed to help traders identify potential short and long opportunities based on candle structure and market momentum. It combines price action analysis with the Williams %R (W%R) oscillator to highlight candles with high potential for reversal or continuation.

Can be used on any timeline, from scalping day trades to swing trades on daily and higher timelines. Know that the higher the timeline the less likely the indicator will show. (Asia and London sessions tend to show many indicators. I find this more useful for NY session.)

How the script works

Candle Structure Conditions

Short (Sell) Wedge: Plotted above green candles that have no bottom wick, indicating that inside that candle there was strong upward momentum without downside hesitation .

Long (Buy) Wedge: Plotted below red candles that have no top wick, indicating that inside that candle there was strong downward momentum without upside hesitation .

These candles are visually emphasized as wedges to mark potential turning points.

Williams %R Filter

The indicator uses Williams %R to measure overbought and oversold conditions:

Proximity to 0 (nearZeroThresh): Determines how close W%R must be to 0 (overbought) to trigger a Sell Wedge. This acts as a “Sell sensitivity” filter.

Proximity to -100 (nearHundredThresh): Determines how close W%R must be to -100 (oversold) to trigger a Buy Wedge. This acts as a “Buy sensitivity” filter.

When the candle meets both the candle structure and the W%R condition, the wedge is plotted in purple (“Within W%R Range”).

When the "ignore W%R filter" toggle is on, all eligible candles are plotted regardless of W%R. Wedges that normally would not meet W%R criteria are plotted in light purple (“Outside W%R Range”) to distinguish them. #YOLO (🚫 I recommend leaving "Ignore W%R Filter" OFF)

Settings Explained

Williams %R Length: The number of bars used to calculate the W%R oscillator. Shorter lengths make it more sensitive; longer lengths smooth the readings.

Proximity to 0 / 100: Controls how “strict” the indicator is in requiring overbought or oversold W%R conditions to trigger. Lower values mean closer to extreme zones, higher values are more permissive.

Ignore W%R Toggle: Option to show Devil’s Marks on every eligible candle regardless of W%R. Useful for visualizing purely price-action-based signals.

What the trader sees

Purple wedges: Candles meeting both candle structure and W%R conditions.

Light purple wedges: Candles meeting candle structure but ignored W%R (when toggle is on). #YOLO (🚫 I recommend leaving "Ignore W%R Filter" OFF)

Short opportunities are wedges above bars (green candles with no bottom wick).

Long opportunities are wedges below bars (red candles with no top wick).

Trading Insight

The Devil’s Mark is a momentum and reversal alert tool:

Look for purple downward-pointing wedges when W%R is near overbought. This is a potential shorting opportunity. Buying at the close of that candle may improve your short trades.

Look for purple upward-pointing wedges when W%R is near oversold. This is a potential

long opportunity. Buying at the close of that candle may improve your long trades.

Light purple wedges show the same price-action cues without W%R confirmation—useful for aggressive traders who want every potential setup. #YOLO #YMMV #noFullPort

Settings / Security

The “Output values” checkbox appears for each plotted series (like a plot or plotshape) and controls whether the series will also be exposed numerically in the Data Window or used by other indicators/scripts.

Here’s what it means in practice:

1. Checked (true)

The series values (like candle high, low, or any computed value) are exported to the Data Window and can be read by other scripts using request.security() or ta functions.

Example: You can see the exact numerical value of each plotted point in the Data Window when you hover over the chart.

Useful if you want to backtest or reference these plotted values programmatically.

2. Unchecked (false)

The series is plotted visually only.

The numeric values are hidden from the Data Window and cannot be accessed by other scripts.

Makes the chart cleaner if you don’t need the numeric outputs.

Nef33 Forex & Crypto Trading Signals PRO

1. Understanding the Indicator's Context

The indicator generates signals based on confluence (trend, volume, key zones, etc.), but it does not include predefined SL or TP levels. To establish them, we must:

Use dynamic or static support/resistance levels already present in the script.

Incorporate volatility (such as ATR) to adjust the levels based on market conditions.

Define a risk/reward ratio (e.g., 1:2).

2. Options for Determining SL and TP

Below, I provide several ideas based on the tools available in the script:

Stop Loss (SL)

The SL should protect you from adverse movements. You can base it on:

ATR (Volatility): Use the smoothed ATR (atr_smooth) multiplied by a factor (e.g., 1.5 or 2) to set a dynamic SL.

Buy: SL = Entry Price - (atr_smooth * atr_mult).

Sell: SL = Entry Price + (atr_smooth * atr_mult).

Key Zones: Place the SL below a support (for buys) or above a resistance (for sells), using Order Blocks, Fair Value Gaps, or Liquidity Zones.

Buy: SL below the nearest ob_lows or fvg_lows.

Sell: SL above the nearest ob_highs or fvg_highs.

VWAP: Use the daily VWAP (vwap_day) as a critical level.

Buy: SL below vwap_day.

Sell: SL above vwap_day.

Take Profit (TP)

The TP should maximize profits. You can base it on:

Risk/Reward Ratio: Multiply the SL distance by a factor (e.g., 2 or 3).

Buy: TP = Entry Price + (SL Distance * 2).

Sell: TP = Entry Price - (SL Distance * 2).

Key Zones: Target the next resistance (for buys) or support (for sells).

Buy: TP at the next ob_highs, fvg_highs, or liq_zone_high.

Sell: TP at the next ob_lows, fvg_lows, or liq_zone_low.

Ichimoku: Use the cloud levels (Senkou Span A/B) as targets.

Buy: TP at senkou_span_a or senkou_span_b (whichever is higher).

Sell: TP at senkou_span_a or senkou_span_b (whichever is lower).

3. Practical Implementation

Since the script does not automatically draw SL/TP, you can:

Calculate them manually: Observe the chart and use the levels mentioned.

Modify the code: Add SL/TP as labels (label.new) at the moment of the signal.

Here’s an example of how to modify the code to display SL and TP based on ATR with a 1:2 risk/reward ratio:

Modified Code (Signals Section)

Find the lines where the signals (trade_buy and trade_sell) are generated and add the following:

pinescript

// Calculate SL and TP based on ATR

atr_sl_mult = 1.5 // Multiplier for SL

atr_tp_mult = 3.0 // Multiplier for TP (1:2 ratio)

sl_distance = atr_smooth * atr_sl_mult

tp_distance = atr_smooth * atr_tp_mult

if trade_buy

entry_price = close

sl_price = entry_price - sl_distance

tp_price = entry_price + tp_distance

label.new(bar_index, low, "Buy: " + str.tostring(math.round(bull_conditions, 1)), color=color.green, textcolor=color.white, style=label.style_label_up, size=size.tiny)

label.new(bar_index, sl_price, "SL: " + str.tostring(math.round(sl_price, 2)), color=color.red, textcolor=color.white, style=label.style_label_down, size=size.tiny)

label.new(bar_index, tp_price, "TP: " + str.tostring(math.round(tp_price, 2)), color=color.blue, textcolor=color.white, style=label.style_label_up, size=size.tiny)

if trade_sell

entry_price = close

sl_price = entry_price + sl_distance

tp_price = entry_price - tp_distance

label.new(bar_index, high, "Sell: " + str.tostring(math.round(bear_conditions, 1)), color=color.red, textcolor=color.white, style=label.style_label_down, size=size.tiny)

label.new(bar_index, sl_price, "SL: " + str.tostring(math.round(sl_price, 2)), color=color.red, textcolor=color.white, style=label.style_label_up, size=size.tiny)

label.new(bar_index, tp_price, "TP: " + str.tostring(math.round(tp_price, 2)), color=color.blue, textcolor=color.white, style=label.style_label_down, size=size.tiny)

Code Explanation

SL: Calculated by subtracting/adding sl_distance to the entry price (close) depending on whether it’s a buy or sell.

TP: Calculated with a double distance (tp_distance) for a 1:2 risk/reward ratio.

Visualization: Labels are added to the chart to display SL (red) and TP (blue).

4. Practical Strategy Without Modifying the Code

If you don’t want to modify the script, follow these steps manually:

Entry: Take the trade_buy or trade_sell signal.

SL: Check the smoothed ATR (atr_smooth) on the chart or calculate a fixed level (e.g., 1.5 times the ATR). Also, review nearby key zones (OB, FVG, VWAP).

TP: Define a target based on the next key zone or multiply the SL distance by 2 or 3.

Example:

Buy at 100, ATR = 2.

SL = 100 - (2 * 1.5) = 97.

TP = 100 + (2 * 3) = 106.

5. Recommendations

Test in Demo: Apply this logic in a demo account to adjust the multipliers (atr_sl_mult, atr_tp_mult) based on the market (forex or crypto).

Combine with Zones: If the ATR-based SL is too wide, use the nearest OB or FVG as a reference.

Risk/Reward Ratio: Adjust the TP based on your tolerance (1:1, 1:2, 1:3)

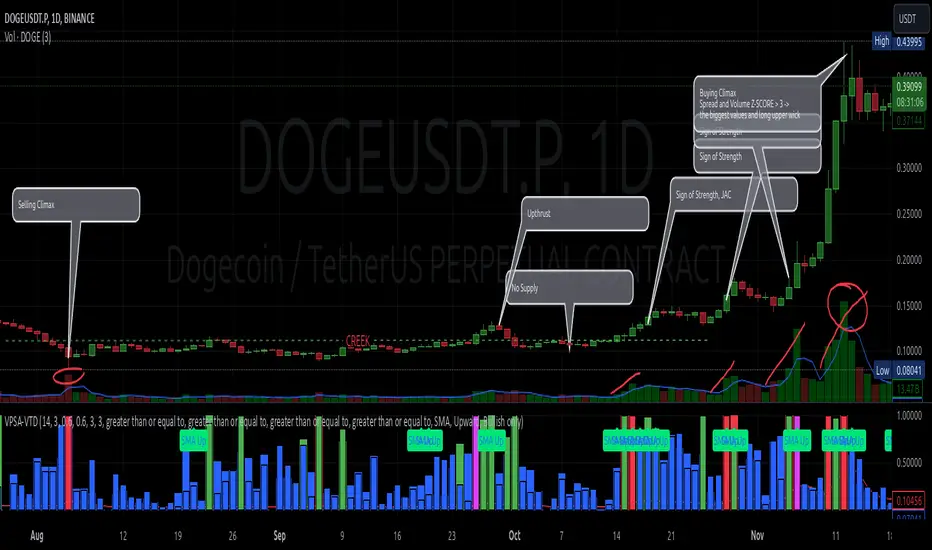

VPSA-VTDDear Sir/Madam,

I am pleased to present the next iteration of my indicator concept, which, in my opinion, serves as a highly useful tool for analyzing markets using the Volume Spread Analysis (VSA) method or the Wyckoff methodology.

The VPSA (Volume-Price Spread Analysis), the latest version in the family of scripts I’ve developed, appears to perform its task effectively. The combination of visualizing normalized data alongside their significance, achieved through the application of Z-Score standardization, proved to be a sound solution. Therefore, I decided to take it a step further and expand my project with a complementary approach to the existing one.

Theory

At the outset, I want to acknowledge that I’m aware of the existence of other probabilistic models used in financial markets, which may describe these phenomena more accurately. However, in line with Occam's Razor, I aimed to maintain simplicity in the analysis and interpretation of the concepts below. For this reason, I focused on describing the data using the Gaussian distribution.

The data I read from the chart — primarily the closing price, the high-low price difference (spread), and volume — exhibit cyclical patterns. These cycles are described by Wyckoff's methodology, while VSA complements and presents them from a different perspective. I will refrain from explaining these methods in depth due to their complexity and broad scope. What matters is that within these cycles, various events occur, described by candles or bars in distinct ways, characterized by different spreads and volumes. When observing the chart, I notice periods of lower volatility, often accompanied by lower volumes, as well as periods of high volatility and significant volumes. It’s important to find harmony within this apparent chaos. I think that chart interpretation cannot happen without considering the broader context, but the more variables I include in the analytical process, the more challenges arise. For instance, how can I determine if something is large (wide) or small (narrow)? For elements like volume or spread, my script provides a partial answer to this question. Now, let’s get to the point.

Technical Overview

The first technique I applied is Min-Max Normalization. With its help, the script adjusts volume and spread values to a range between 0 and 1. This allows for a comparable bar chart, where a wide bar represents volume, and a narrow one represents spread. Without normalization, visually comparing values that differ by several orders of magnitude would be inconvenient. If the indicator shows that one bar has a unit spread value while another has half that value, it means the first bar is twice as large. The ratio is preserved.

The second technique I used is Z-Score Standardization. This concept is based on the normal distribution, characterized by variables such as the mean and standard deviation, which measures data dispersion around the mean. The Z-Score indicates how many standard deviations a given value deviates from the population mean. The higher the Z-Score, the more the examined object deviates from the mean. If an object has a Z-Score of 3, it falls within 0.1% of the population, making it a rare occurrence or even an anomaly. In the context of chart analysis, such strong deviations are events like climaxes, which often signal the end of a trend, though not always. In my script, I assigned specific colors to frequently occurring Z-Score values:

Below 1 – Blue

Above 1 – Green

Above 2 – Red

Above 3 – Fuchsia

These colors are applied to both spread and volume, allowing for quick visual interpretation of data.

Volume Trend Detector (VTD)

The above forms the foundation of VPSA. However, I have extended the script with a Volume Trend Detector (VTD). The idea is that when I consider market structure - by market structure, I mean the overall chart, support and resistance levels, candles, and patterns typical of spread and volume analysis as well as Wyckoff patterns - I look for price ranges where there is a lack of supply, demand, or clues left behind by Smart Money or the market's enigmatic identity known as the Composite Man. This is essential because, as these clues and behaviors of market participants — expressed through the chart’s dynamics - reflect the actions, decisions, and emotions of all players. These behaviors can help interpret the bull-bear battle and estimate the probability of their next moves, which is one of the key factors for a trader relying on technical analysis to make a trade decision.

I enhanced the script with a Volume Trend Detector, which operates in two modes:

Step-by-Step Logic

The detector identifies expected volume dynamics. For instance, when looking for signs of a lack of bullish interest, I focus on setups with decreasing volatility and volume, particularly for bullish candles. These setups are referred to as No Demand patterns, according to Tom Williams' methodology.

Simple Moving Average (SMA)

The detector can also operate based on a simple moving average, helping to identify systematic trends in declining volume, indicating potential imbalances in market forces.

I’ve designed the program to allow the selection of candle types and volume characteristics to which the script will pay particular attention and notify me of specific market conditions.

Advantages and Disadvantages

Advantages:

Unified visualization of normalized spread and volume, saving time and improving efficiency.

The use of Z-Score as a consistent and repeatable relative mechanism for marking examined values.

The use of colors in visualization as a reference to Z-Score values.

The possibility to set up a continuous alert system that monitors the market in real time.

The use of EMA (Exponential Moving Average) as a moving average for Z-Score.

The goal of these features is to save my time, which is the only truly invaluable resource.

Disadvantages:

The assumption that the data follows a normal distribution, which may lead to inaccurate interpretations.

A fixed analysis period, which may not be perfectly suited to changing market conditions.

The use of EMA as a moving average for Z-Score, listed both as an advantage and a disadvantage depending on market context.

I have included comments within the code to explain the logic behind each part. For those who seek detailed mathematical formulas, I invite you to explore the code itself.

Defining Program Parameters:

Numerical Conditions:

VPSA Period for Analysis – The number of candles analyzed.

Normalized Spread Alert Threshold – The expected normalized spread value; defines how large or small the spread should be, with a range of 0-1.00.

Normalized Volume Alert Threshold – The expected normalized volume value; defines how large or small the volume should be, with a range of 0-1.00.

Spread Z-SCORE Alert Threshold – The Z-SCORE value for the spread; determines how much the spread deviates from the average, with a range of 0-4 (a higher value can be entered, but from a logical standpoint, exceeding 4 is unnecessary).

Volume Z-SCORE Alert Threshold – The Z-SCORE value for volume; determines how much the volume deviates from the average, with a range of 0-4 (the same logical note as above applies).

Logical Conditions:

Logical conditions describe whether the expected value should be less than or equal to or greater than or equal to the numerical condition.

All four parameters accept two possibilities and are analogous to the numerical conditions.

Volume Trend Detector:

Volume Trend Detector Period for Analysis – The analysis period, indicating the number of candles examined.

Method of Trend Determination – The method used to determine the trend. Possible values: Step by Step or SMA.

Trend Direction – The expected trend direction. Possible values: Upward or Downward.

Candle Type – The type of candle taken into account. Possible values: Bullish, Bearish, or Any.

The last available setting is the option to enable a joint alert for VPSA and VTD.

When enabled, VPSA will trigger on the last closed candle, regardless of the VTD analysis period.

Example Use Cases (Labels Visible in the Script Window Indicate Triggered Alerts):

The provided labels in the chart window mark where specific conditions were met and alerts were triggered.

Summary and Reflections

The program I present is a strong tool in the ongoing "game" with the Composite Man.

However, it requires familiarity and understanding of the underlying methodologies to fully utilize its potential.

Of course, like any technical analysis tool, it is not without flaws. There is no indicator that serves as a perfect Grail, accurately signaling Buy or Sell in every case.

I would like to thank those who have read through my thoughts to the end and are willing to take a closer look at my work by using this script.

If you encounter any errors or have suggestions for improvement, please feel free to contact me.

I wish you good health and accurately interpreted market structures, leading to successful trades!

CatTheTrader

Previous 5 Day Market CloseThis indicator can be used with a strategy known as gap close reversal. Gap close reversal is a trading strategy based on the idea that when a market experiences a gap (a significant difference between the previous day's close and the current day's open), there's a tendency for the price to fill or "close" the gap by moving back to the previous day's closing price. Traders often look for such opportunities as potential entry or exit points.

Here's how you can use this script for gap close reversal trading:

Identify Gaps: Look for instances where the current day's open price significantly deviates from the previous day's close, resulting in a gap on the chart. This could be a gap-up (where the open is higher than the previous close) or a gap-down (where the open is lower than the previous close).

Plot the Script: Apply the "Past 5 Days Close" script to your chart. This will plot the closing prices of the past five trading days as lines on the chart. These lines will serve as reference points for potential gap close levels.

Look for Reversal Signals: Monitor the price action as the market opens and observe how it behaves in relation to the previous day's close and the lines plotted by the script. If the price starts to move towards one of the past closing prices after a gap, it could indicate a potential reversal.

Confirm with Other Indicators: Use additional technical indicators or chart patterns to confirm the potential reversal signal. For example, you might look for bullish or bearish candlestick patterns, support or resistance levels, or momentum indicators aligning with the reversal.

Advanced Dynamic Threshold RSI [Elysian_Mind]Advanced Dynamic Threshold RSI Indicator

Overview

The Advanced Dynamic Threshold RSI Indicator is a powerful tool designed for traders seeking a unique approach to RSI-based signals. This indicator combines traditional RSI analysis with dynamic threshold calculation and optional Bollinger Bands to generate weighted buy and sell signals.

Features

Dynamic Thresholds: The indicator calculates dynamic thresholds based on market volatility, providing more adaptive signal generation.

Performance Analysis: Users can evaluate recent price performance to further refine signals. The script calculates the percentage change over a specified lookback period.

Bollinger Bands Integration: Optional integration of Bollinger Bands for additional confirmation and visualization of potential overbought or oversold conditions.

Customizable Settings: Traders can easily customize key parameters, including RSI length, SMA length, lookback bars, threshold multiplier, and Bollinger Bands parameters.

Weighted Signals: The script introduces a unique weighting mechanism for signals, reducing false positives and improving overall reliability.

Underlying Calculations and Methods

1. Dynamic Threshold Calculation:

The heart of the Advanced Dynamic Threshold RSI Indicator lies in its ability to dynamically calculate thresholds based on multiple timeframes. Let's delve into the technical details:

RSI Calculation:

For each specified timeframe (1-hour, 4-hour, 1-day, 1-week), the Relative Strength Index (RSI) is calculated using the standard 14-period formula.

SMA of RSI:

The Simple Moving Average (SMA) is applied to each RSI, resulting in the smoothing of RSI values. This smoothed RSI becomes the basis for dynamic threshold calculations.

Dynamic Adjustment:

The dynamically adjusted threshold for each timeframe is computed by adding a constant value (5 in this case) to the respective SMA of RSI. This dynamic adjustment ensures that the threshold reflects changing market conditions.

2. Weighted Signal System:

To enhance the precision of buy and sell signals, the script introduces a weighted signal system. Here's how it works technically:

Signal Weighting:

The script assigns weights to buy and sell signals based on the crossover and crossunder events between RSI and the dynamically adjusted thresholds. If a crossover event occurs, the weight is set to 2; otherwise, it remains at 1.

Signal Combination:

The weighted buy and sell signals from different timeframes are combined using logical operations. A buy signal is generated if the product of weights from all timeframes is equal to 2, indicating alignment across timeframe.

3. Experimental Enhancements:

The Advanced Dynamic Threshold RSI Indicator incorporates experimental features for educational exploration. While not intended as proven strategies, these features aim to offer users a glimpse into unconventional analysis. Some of these features include Performance Calculation, Volatility Calculation, Dynamic Threshold Calculation Using Volatility, Bollinger Bands Module, Weighted Signal System Incorporating New Features.

3.1 Performance Calculation:

The script calculates the percentage change in the price over a specified lookback period (variable lookbackBars). This provides a measure of recent performance.

pctChange(src, length) =>

change = src - src

pctChange = (change / src ) * 100

recentPerformance1H = pctChange(close, lookbackBars)

recentPerformance4H = pctChange(request.security(syminfo.tickerid, "240", close), lookbackBars)

recentPerformance1D = pctChange(request.security(syminfo.tickerid, "1D", close), lookbackBars)

3.2 Volatility Calculation:

The script computes the standard deviation of the closing price to measure volatility.

volatility1H = ta.stdev(close, 20)

volatility4H = ta.stdev(request.security(syminfo.tickerid, "240", close), 20)

volatility1D = ta.stdev(request.security(syminfo.tickerid, "1D", close), 20)

3.3 Dynamic Threshold Calculation Using Volatility:

The dynamic thresholds for RSI are calculated by adding a multiplier of volatility to 50.

dynamicThreshold1H = 50 + thresholdMultiplier * volatility1H

dynamicThreshold4H = 50 + thresholdMultiplier * volatility4H

dynamicThreshold1D = 50 + thresholdMultiplier * volatility1D

3.4 Bollinger Bands Module:

An additional module for Bollinger Bands is introduced, providing an option to enable or disable it.

// Additional Module: Bollinger Bands

bbLength = input(20, title="Bollinger Bands Length")

bbMultiplier = input(2.0, title="Bollinger Bands Multiplier")

upperBand = ta.sma(close, bbLength) + bbMultiplier * ta.stdev(close, bbLength)

lowerBand = ta.sma(close, bbLength) - bbMultiplier * ta.stdev(close, bbLength)

3.5 Weighted Signal System Incorporating New Features:

Buy and sell signals are generated based on the dynamic threshold, recent performance, and Bollinger Bands.

weightedBuySignal = rsi1H > dynamicThreshold1H and rsi4H > dynamicThreshold4H and rsi1D > dynamicThreshold1D and crossOver1H

weightedSellSignal = rsi1H < dynamicThreshold1H and rsi4H < dynamicThreshold4H and rsi1D < dynamicThreshold1D and crossUnder1H

These features collectively aim to provide users with a more comprehensive view of market dynamics by incorporating recent performance and volatility considerations into the RSI analysis. Users can experiment with these features to explore their impact on signal accuracy and overall indicator performance.

Indicator Placement for Enhanced Visibility

Overview

The design choice to position the "Advanced Dynamic Threshold RSI" indicator both on the main chart and beneath it has been carefully considered to address specific challenges related to visibility and scaling, providing users with an improved analytical experience.

Challenges Faced

1. Differing Scaling of RSI Results:

RSI values for different timeframes (1-hour, 4-hour, and 1-day) often exhibit different scales, especially in markets like gold.

Attempting to display these RSIs on the same chart can lead to visibility issues, as the scaling differences may cause certain RSI lines to appear compressed or nearly invisible.

2. Candlestick Visibility vs. RSI Scaling:

Balancing the visibility of candlestick patterns with that of RSI values posed a unique challenge.

A single pane for both candlesticks and RSIs may compromise the clarity of either, particularly when dealing with assets that exhibit distinct volatility patterns.

Design Solution

Placing the buy/sell signals above/below the candles helps to maintain a clear association between the signals and price movements.

By allocating RSIs beneath the main chart, users can better distinguish and analyze the RSI values without interference from candlestick scaling.

Doubling the scaling of the 1-hour RSI (displayed in blue) addresses visibility concerns and ensures that it remains discernible even when compared to the other two RSIs: 4-hour RSI (orange) and 1-day RSI (green).

Bollinger Bands Module is optional, but is turned on as default. When the module is turned on, the users can see the upper Bollinger Band (green) and lower Bollinger Band (red) on the main chart to gain more insight into price actions of the candles.

User Flexibility

This dual-placement approach offers users the flexibility to choose their preferred visualization:

The main chart provides a comprehensive view of buy/sell signals in relation to candlestick patterns.

The area beneath the chart accommodates a detailed examination of RSI values, each in its own timeframe, without compromising visibility.

The chosen design optimizes visibility and usability, addressing the unique challenges posed by differing RSI scales and ensuring users can make informed decisions based on both price action and RSI dynamics.

Usage

Installation

To ensure you receive updates and enhancements seamlessly, follow these steps:

Open the TradingView platform.

Navigate to the "Indicators" tab in the top menu.

Click on "Community Scripts" and search for "Advanced Dynamic Threshold RSI Indicator."

Select the indicator from the search results and click on it to add to your chart.

This ensures that any future updates to the indicator can be easily applied, keeping you up-to-date with the latest features and improvements.

Review Code

Open TradingView and navigate to the Pine Editor.

Copy the provided script.

Paste the script into the Pine Editor.

Click "Add to Chart."

Configuration

The indicator offers several customizable settings:

RSI Length: Defines the length of the RSI calculation.

SMA Length: Sets the length of the SMA applied to the RSI.

Lookback Bars: Determines the number of bars used for recent performance analysis.

Threshold Multiplier: Adjusts the multiplier for dynamic threshold calculation.

Enable Bollinger Bands: Allows users to enable or disable Bollinger Bands integration.

Interpreting Signals

Buy Signal: Generated when RSI values are above dynamic thresholds and a crossover occurs.

Sell Signal: Generated when RSI values are below dynamic thresholds and a crossunder occurs.

Additional Information

The indicator plots scaled RSI lines for 1-hour, 4-hour, and 1-day timeframes.

Users can experiment with additional modules, such as machine-learning simulation, dynamic real-life improvements, or experimental signal filtering, depending on personal preferences.

Conclusion

The Advanced Dynamic Threshold RSI Indicator provides traders with a sophisticated tool for RSI-based analysis, offering a unique combination of dynamic thresholds, performance analysis, and optional Bollinger Bands integration. Traders can customize settings and experiment with additional modules to tailor the indicator to their trading strategy.

Disclaimer: Use of the Advanced Dynamic Threshold RSI Indicator

The Advanced Dynamic Threshold RSI Indicator is provided for educational and experimental purposes only. The indicator is not intended to be used as financial or investment advice. Trading and investing in financial markets involve risk, and past performance is not indicative of future results.

The creator of this indicator is not a financial advisor, and the use of this indicator does not guarantee profitability or specific trading outcomes. Users are encouraged to conduct their own research and analysis and, if necessary, consult with a qualified financial professional before making any investment decisions.

It is important to recognize that all trading involves risk, and users should only trade with capital that they can afford to lose. The Advanced Dynamic Threshold RSI Indicator is an experimental tool that may not be suitable for all individuals, and its effectiveness may vary under different market conditions.

By using this indicator, you acknowledge that you are doing so at your own risk and discretion. The creator of this indicator shall not be held responsible for any financial losses or damages incurred as a result of using the indicator.

Kind regards,

Ely

A_Taders_Edge_LIBRARYLibrary "A_Taders_Edge_LIBRARY"

RCI(_rciLength, _close, _interval, _outerMostRangeOfOscillator)

- You will see me using this a lot. DEFINITELY my favorite oscillator to utilize for SO many different things from timing entries/exits to determining trends.

Parameters:

_rciLength (int)

_close (float)

_interval (int)

_outerMostRangeOfOscillator (int)

Returns: - Outputs a single RCI value that will between (-)_outerMostRangeOfOscillator to (+)_outerMostRangeOfOscillator

InvalidTID(_close, _showInvalidAssets, _securityTickerid, _invalidArray)

- This is to add a table on the right of your chart that prints all the TickerID's that were either not formulated correctly in the scripts input or that is not a valid symbol and should be changed.

Parameters:

_close (float)

_showInvalidAssets (simple bool)

_securityTickerid (string)

_invalidArray (string )

Returns: - Does NOT return a value but rather the table with the invalid TickerID's from the scripts input that need to be changed.

LabelLocation(_firstLocation)

- This is ONLY for when you are wanting to print ALERT LABELS with the assets name for when an alert trigger occurs for that asset. There are a total of 40 assets that can be used in each copy of the script. You don't want labels from different assets printing on top of each other because you will not be able to read the asset name that the label is for. Ex. If you put your _firstLocation in the input settings as 1 and have 40 assets on this copy of the scanner then the first asset in the list is assigned to the location value 1 on the scale, and the 2nd in the list is assigned to location value 2...and so on. If your first location is set to 81 then the 1st asset is 81 and 2nd is 82 and so on.

Parameters:

_firstLocation (simple int)

Returns: - regardless of if you have the maximum amount of assets being screened (40 max), this export function will output 40 locations… So there needs to be 40 variables assigned to the tuple in this export function. What I mean by that is there needs to be 40 variables between the ' '. If you only have 20 assets in your scripts input settings, then only the first 20 variables within the ' ' Will be assigned to a value location and the other 20 will be assigned 'NA'.

SeparateTickerids(_string)

- You must form this single tickerID input string exactly as laid out in the water (a little gray circle at the end of the setting, that you hover your cursor over to read the details of). IF the string is formed correctly then it will break up. All of the tip rate is within the string into a total of 40 separate strings which will be all of the tickerIDs that the script is using in your MO scanner.

Parameters:

_string (simple string)

Returns: - this will output, 40 different security assets within the tuple output (ie. 40 variable within the ' ') regardless of if you were including 40 assets, to be screened in the MO Screener or not. if you have less than 40 assets, then once the variables are assigned to all of the tickerIDs, the rest of the variables will be assigned "NA".

TickeridForLabelsAndSecurity(_includeExchange, _ticker)

- this export function is used to output 2 tickerID strings. One is formulated to properly work in the request.security() function while the other is how it will appear on the asset name labels depending on how you form your assets string in the MO scanners input settings. Review the tooltip next to the setting, to learn how to form the string so that the asset name labels will appear how you want in the labels at the end of the line plots & the alert labels that would be triggered if the MO Scanner is set up to include Alert Trigger Labels.

Parameters:

_includeExchange (simple bool)

_ticker (simple string)

Returns: - this export function is used to output 2 tickerID strings. One is formulated to properly work in the request.security() function while the other is how it will appear on the asset name labels depending on how you form your assets string in the MO scanners input settings. Review the tooltip next to the setting, to learn how to form the string so that the asset name labels will appear how you want in the labels at the end of the line plots & the alert labels that would be triggered if the MO Scanner is set up to include Alert Trigger Labels.

PercentChange(_startingValue, _endingValue)

- this is a quick export function to calculate how much % change has occurred between the _startingValue and the _endingValue that you input into the export function.

Parameters:

_startingValue (float)

_endingValue (float)

Returns: - it will output a single percentage value between 0-100 with trailing numbers behind a decimal. If you want, only a certain amount of numbers behind the decimal, this export function needs to be put within a formatting function to do so. Explained in the MO Scanner INTRO VIDEO.

PrintedBarCount(_time, _barCntLength, _bcPmin)

- This export function will outfit the percentage of printed bars (that occurred within _barCntLength amount of time) out of the MAX amount of bars that potentially COULD HAVE been printed. Iexplanation in the MO Scanner INTRO VIDEO.

Parameters:

_time (int)

_barCntLength (int)

_bcPmin (int)

Returns: - Gives 2 outputs. The first is the total % of Printed Bars within the user set time period and second is true/false according to if the Printed BarCount % is above the _bcPmin threshold that you input into this export function.

Trend Reversal System with SR levelsHello All,

This is the Trend Reversal System with Support/Resistance levels script. long time ago I published it as closed source but now I upgraded it and and published as open-source with a different name. I hope it would be useful for you all while trading/analyzing.

The script has some parts in it: Setup, Count, SR levels, Risk levels & Targets . Now lets check them:

Setup Part: it has two part, Buy or Sell Setup. one of them can be active only. Buy setup: if current close checks if current is lower/equal than the close of the 5. bar. if yes then the script increases number of buy setup. and if it reaches 9 then the script checks if current low is lower/equal than the lows of last 3. and 4. bars, or if the low of the last bar is lower/equal than the lows of last 3. and 4. bars. if yes then the script increases the buy setup by 1. if these conditions met then it puts the label 'S' , same for Sell setup. S labels on both setup are potential reversals.

Count Part: If buy or sell setup reaches the 9 then Count part starts from 1. lets see buy count: If current close is lower/equal than the low of the 3. bar and buy count is lower than 12 or low of the bar 13 is less than or equal to the close of bar 8 then buy count increase or it's completed. if it's completed then the script puts C label, and it's potential reversal. of course there are some conditions that can cancel the count buy/sell or recycle/restart.

By using Setup and Count levels the script can show Support/Resistance Levels, Risk levels & Targets. SR levels are potential reversal levels.

Lets see some example screenshots:

Support/Resistance levels:

Potential Reversal levels and how setup/counts are shown:

Count part can recycle and the script shows it as 'R' , ( you can see the conditions for Recycle in the script ):

Count can be cancelled and and it's shown as 'x'

If the scripts find 9 on Setup or 13 on Count then it checks if it's a good level to buy/sell and if it decides it's good level then it shows TRSSetup Buy/Sell or TRSCount Buy/Sell and also shows the target. in following example the script checks and decide it's a good level to take long position. it can be aggressive or conservative, Conservative is recommended.

Enjoy!

Tick StatisticsTick Statistics:

I have seen many questions/queries related to tick data in TV telegram channels. This script will help pine scripts to understand how ticks work, how to capture and process tick data.

This is an educational indicator script for pine scripters.

The indicator shall work only on real time candles. Tick data capture is initiated as soon as indicator is loaded on the chart. You might not get correct statistics on 1st candle in case indicator is loaded when real time candle is in progress, in such case you can monitor the statistics generated for subsequent candles.

Generated statistics is shown on the chart by placing 2 diamond shapes above and below the candle.

Diamond shape below the candle will have candles ‘tick data’ listed in a table. This can be view by placing mouse pointer on the diamond shape. Refer to point 1 below for more details.

Diamond shape above the candle will have statistics as mentioned in point no 2 onwards. To view the statistics place the mouse point on the diamond shape. The shape will appear in green color when both tick price and tick volume are both moving in the same direction. The diamond shape in red color means tick price and tick volume are moving in opposite direction.

The script captures tick by tick data and generate statistics below:

1. List of tick data with details below: (this is stored in the diamond shape placed below the candle)

a. Tick no

b. Tick type – Up tick (Up), Down tick (Dn), No change (--)

c. Tick price

d. Volume

e. Price difference (as compared to previous tick price)

f. Volume difference (as compared to previous tick volume)

2. Tick statistics

a. Total ticks

b. Number of up ticks

c. Number of down ticks

d. Number of No change ticks

3. Volume Statistics

a. Total volume

b. Up tick volume

c. Down tick volume

d. Volume associated with ticks where there is no change

e. Candle volume (just for reconciliation purpose)

4. Max-min statistics

a. Max volume = <> at price = <> at tick no = <>

b. Min volume = <> at price = <> at tick no = <>

c. Max price = <> at volume = <> at tick no = <>

d. Min price = <> at volume = <> at tick no = <>

5. Candle summary

a. Price << Up >> (if price is up as compared to 1st tick <> otherwise

b. Volume <> (if up tick volume is more than down tick volume <> otherwise

Fair Value Gap [LuxAlgo]Fair value gaps (FVG) highlight imbalances areas between market participants and have become popular amongst technical analysts. The following script aims to display fair value gaps alongside the percentage of filled gaps and the average duration (in bars) before gaps are filled.

Users can be alerted when an FVG is filled using the alerts built into this script.

🔶 USAGE

In practice, FVG's highlight areas of support (bullish FVG) and resistances (bearish FVG). Once a gap is filled, suggesting the end of the imbalance, we can expect the price to reverse.

This approach is more contrarian in nature, users wishing to use a more trend-following approach can use the identification of FVG as direct signals, going long with the identification of a bullish FVG, and short with a bearish FVG.

🔹 Mitigation

By default, the script highlights the areas of only unmitigated FVG's. Users can however highlight the mitigation level of mitigated FVG's, that is the lower extremity of bullish FVG's and the upper extremity of bearish FVG's.

The user can track the evolution of a mitigated FVG's using the "Dynamic" setting.

🔹 Threshold

The gap height can be used to determine the degree of imbalance between buying and selling market participants. Users can filter fair value gaps based on the gap height using the "Threshold %" setting. Using the "Auto" will make use of an automatic threshold, only keeping more volatile FVG's.

🔶 DETAILS

We use the following rules for detecting FVG's in this script:

Bullish FVG

low > high(t-2)

close(t-1) > high(t-2)

(low - high(t-2)) / high(t-2) > threshold

Upper Bullish FVG = low

Lower Bullish FVG = high(t-2)

Bearish FVG

high < low(t-2)

close(t-1) < low(t-2)

(low(t-2) - high) / high < -threshold

Upper Bearish FVG = low(t-2)

Lower Bearish FVG = high

🔶 SETTINGS

Threshold %: Threshold percentage used to filter our FVG's based on their height.

Auto Threshold: Use the cumulative mean of relative FVG heights as threshold.

Unmitigatted Levels: Extent the mitigation level of the number of unmitigated FVG's set by the user.

Mitigation Levels: Show the mitigation levels of mitigated FVG's.

Timeframe : Timeframe of the price data used to detect FVG's.

KCGmut“KCGmut” stands for “Mutations Of Keltner Center Of Gravity Channel”.

After adding the ‘KeltCOG Width’ label to the KeltCOG, I got the idea of creating a subpanel indicator to show the development of the width-percent in previous periods. After some more thinking, I decided that the development of the COG-width-percent should also be reported and somehow the indicator should report whether the close is over (momentum is up), in (momentum is sideways) or under (momentum is down) the COG ( This is the gray area in the channel).

Borrowing from other scripts:

I tweeked the script of the KeltCOG (published) to calculate the columns and of REVE (also published) to calculate the volume spikes. Because the KeltCOG script had the default option to let the script chose lookback and adapt the width, I decided to not provide inputs to tweek lookback or channel width. Thus, if you use a KeltCOG in default setting, REVE and KCGmut together in the same chart, these will provide consistent complementary information about the candle. This layout has this combination:

I added actual volume to show where volume spikes occur.

Columns

For the channel-width-percent half of the value is used and for the COG-width-percent the whole to get a better image

By plotting the columns of the full width before those of the COG, in two series of positive and negative values, I created the illusion of a column with a different colored patch representing the COG (most are black) at the bottom where it points up (showing momentum is up), in the middle when the close is in the COG (no momentum) or at the top when the close is below the COG (showing momentum is down)

coloring drama

When nothing much happens, i.e. the channels keep the same width of shrink a bit, the columns get an unobtrusive color, black for the small COG patches and bluish gray for the channel columns pointing up or sideways, reddish gray when pointing down. If the COG increases (drama) the patches get colored lime (up), red (down) or orange (sideways, very seldom). If the channel increases, the columns get colored gold (up), maroon (down) or orange (sideways). Because the COG is derived from a Donchian channel, drama means a new high or low in the lookback period. Drama in the KeltCOG channel just means increase in volatility.

histogram showing volume spikes

Blue spikes indicate more then twice as much volume then recently normal, Maroon spikes indicate clear increases less then twice. To prevent the histogram from disappearing behind a column it is plotted first, spikes made longer then the column and also plotted both positive and negative. Single volume spikes don’t mean much, however if these occur in consecutive series and also come together with drama like new highs or increase in volatility, volume is worth noting. I regard such events as ‘voting’, the market ‘votes’ up or down. The REVE analyses these events to asses whether the volume stems from huge institutional traders (‘whales’) or large numbers of small traders (‘muppets’). This might be interesting too.

Remarks about momentum

Like in MACD, momentum has a direction. The difference is that in KCGmut momentum is a choise of the market to move above the COG (uptrend) or in (sideways) or under (downtrend), whereas in MACD the indicator shows the energy with which the market moves up or down. How does the market ‘choose’? The market doesn’t ‘think’, but still it comes to decisions. I see an analogy with the way a swarm of birds decides to go here or there, up or down, or land in a tree. All birds seem to agree but I guess a single bird has not much say in what the swarm does.

LibraryStopwatchLibrary "LibraryStopwatch"

Provides functions to time the execution of a script.

When timing scripts, keep in mind that the runtime environment is fluid on TradingView. Different servers or server loads will impact execution time.

Look first. Then leap.

stopwatchStats() Times the execution of a script.

Returns: A tuple of four values: timePerBarInMs, totalTimeInMs, barsTimed, barsNotTimed

stopwatch() Times the execution of a script.

Returns: A single value: The time elapsed since the beginning of the script, in ms.

Funamental and financialsEarnings and Quarterly reporting and fundamental data at a glance.

A study of the financial data available by the "financial" functions in pinescript/tradingview

As far as I know, this script is unique. I found very few public examples of scripts using the fundamental data. and none that attempt to make the data available in a useful form

as an indicator / chart data. The only fitting category when publishing would be "trend analysis" We are going to look at the trend of the quarterly reports.

The intent is to create an indicator that instantly show the financial health of a company, and the trends in debt, cash and earnings

Normal settings displays all information on a per share basis, and should be viewed on a Daily chart

Percentage of market valuation can be used to compare fundamentals to current share price.

And actual to show the full numbers for verification with quarterly reporting and debuggging (actual is divided by 1.000.000 to keep numbers readable)

Credits to research study by Alex Orekhov (everget) for the Symbol Info Helper script

without it this would still be an unpublished mess, the use of textboxes allow me to remove many squiggly plot lines of fundamental data

Known problems and annoyances

1. Takes a long time to load. probably the amount of financial calls is the culprit. AFAIK not something i can to anything about in the script.

2. Textboxes crowd each other. dirty fix with hardcoded offsets. perhaps a few label offset options in the settings would do?

3. Only a faint idea of how to put text boxes on every quarter. Need time... (pun intended)

Have fun, and if you make significant improvements on this, please publish, or atleast leave a comment or message so I can consider adding it to this script.

© sjakk 2020-june-08

Forex session - Opening Range- Jayy fixed updatedOpening Range (OR) for Forex 24 hour regular session. This is not for regular market day sessions addressed in a separate script.

This script fixes four issues:

syntax error when code compiles

messed up opening range the day after a holiday Monday

flaky plotting of the opening range and targets that required page reloading

TradingView problems with starting forex session at 1700 hours EST/EDT when using certain securities eg FX_IDC currently (Jan 2017)

Additions in his code are more options for trading range

Time compensation option for some securities that incorrectly start sessions at 1200 hrs instead of 1700 hrs NY time

- this glitch is likely temporary but present when this script update was created

More opening range time period choices

Opening Range Targets:

Opening Range Targets as per Leaf_West

Targets are set at 127% , 162%, 200 %, 262 %, 362%, 423%, 685%, 1109% and 1794% and this can be traded intraday using methods described here charts-by-leaf.com I also have some Leaf West PDFs that describe how the targets are set and how they are traded. There are others that use opening range.

The Time Session Glitch and the Fix:

The script will correctly default to 1700 hrs to 1700hrs EDT/EST session for FXCM.

Strangely some securities appear to erroneously start their session at 1200 hrs ie. My guess is that they are somehow tied to GMT+0 instead of New York time (GMT+5). See this for yourself by selecting EURUSD using the FXCM exchange (FX:EURUSD) and then EURUSD from the IDC exchange (FX_IDC:EURUSD). The FX-IDC session opening range starts 5 hours

before it actually should at 1700 hrs EDT/EST. To correct for this I have implemented an automatic fix (default) and a user selected "5 hour time shift adjust. ment needed on some securities".

There is also a 4 hour time shift button which might be necessary when New York reverts from Eastern Standard Time

to Eastern Daylight Time (1 hour difference) in March (and then back again in November). In the default auto adjust mode you will need to select the 1 hour time shift. That is if this glitch still exists at that time.

I have looked at other scripts, other than my own and where the script is available, that need to use information about the opening bar and all have the same time shift issue

What are the choices for Opening Range?

The dialogue box offers the standard TradingView options.

Also where you see Pick Opening Range 1 to 12 hours , SET TO 0 To USE LINE ABOVE TO DETERMINE OR LENGTH

As the note says a number other than 0 will override the standard options from the line above

The dialogue box below in offers choices by hours 1 to 12. A number greater than 12 will still only give

720 minutes (12 hours) for the length of Opening Range.

What sessions within the FOREX time-frame are available?

The default is 1700 hours to 1700 hours EST/EDT

Check any one (only one) of the time periods to change the opening range period to suit.

New York opens at 8:00 am to 5:00 pm EST (EDT)

Tokyo opens at 7:00 pm to 4:00 am EST (EDT)

Sydney opens at 5:00 pm to 2:00 am EST (EDT)

London opens at 3:00 am to 12:00 noon EST (EDT)

There is a build your own session (click the button to select)

The two lines for inputting session times are almost identical except that the second line starts the be the same as each other.

The default for the build your own session is 2200 hours to 2200 hours. As of the time of publishing this plots EURUSD FX-IDC just right. The GMT+5 and GMT+4 do not apply to this selection.

See my comments above on this strange aberration.

The script originated from work done by Chris Moody. It has changed significantly but there are remnants of that script lurking within.

Script is free to all - that way you can see what is inside

Cheers Jayy

CoreMACDHTF [CHE]Library "CoreMACDHTF"

calc_macd_htf(src, preset_str, smooth_len)

Parameters:

src (float)

preset_str (simple string)

smooth_len (int)

is_hist_rising(src, preset_str, smooth_len)

Parameters:

src (float)

preset_str (simple string)

smooth_len (int)

hist_rising_01(src, preset_str, smooth_len)

Parameters:

src (float)

preset_str (simple string)

smooth_len (int)

CoreMACDHTF — Hardcoded HTF MACD Presets with Smoothed Histogram Regime Flags

Summary

CoreMACDHTF provides a reusable MACD engine that approximates higher-timeframe behavior by selecting hardcoded EMA lengths based on the current chart timeframe, then optionally smoothing the resulting histogram with a stateful filter. It is published as a Pine v6 library but intentionally includes a minimal demo plot so you can validate behavior directly on a chart. The primary exported outputs are MACD, signal, a smoothed histogram, and the resolved lengths plus a timeframe tag. In addition, it exposes a histogram rising condition so importing scripts can reuse the same regime logic instead of re-implementing it.

Motivation: Why this design?

Classic MACD settings are often tuned to one timeframe. When you apply the same parameters to very different chart intervals, the histogram can become either too noisy or too sluggish. This script addresses that by using a fixed mapping from the chart timeframe into a precomputed set of EMA lengths, aiming for more consistent “tempo” across intervals. A second problem is histogram micro-chop around turning points; the included smoother reduces short-run flips so regime-style conditions can be more stable for alerts and filters.

What’s different vs. standard approaches?

Reference baseline: a standard MACD using fixed fast, slow, and signal lengths on the current chart timeframe.

Architecture differences:

Automatic timeframe bucketing that selects a hardcoded length set for the chosen preset.

Two preset families: one labeled A with lengths three, ten, sixteen; one labeled B with lengths twelve, twenty-six, nine.

A custom, stateful histogram smoother intended to damp noisy transitions.

Library exports that return both signals and metadata, plus a dedicated “histogram rising” boolean.

Practical effect:

The MACD lengths change when the chart timeframe changes, so the oscillator’s responsiveness is not constant across intervals by design.

The rising-flag logic is based on the smoothed histogram, which typically reduces single-bar flip noise compared to using the raw histogram directly.

How it works (technical)

1. The script reads the chart timeframe and converts it into milliseconds using built-in timeframe helpers.

2. It assigns the timeframe into a bucket label, such as an intraday bucket or a daily-and-above bucket, using fixed thresholds.

3. It resolves a hardcoded fast, slow, and signal length triplet based on:

The selected preset family.

The bucket label.

In some cases, the current minute multiplier for finer mapping.

4. It computes fast and slow EMAs on the selected source and subtracts them to obtain MACD, then computes an EMA of MACD for the signal line.

5. The histogram is derived from the difference between MACD and signal, then passed through a custom smoother.

6. The smoother uses persistent internal state to carry forward its intermediate values from bar to bar. This is intentional and means the smoothing output depends on contiguous bar history.

7. The histogram rising flag compares the current smoothed histogram to its prior value. On the first comparable bar it defaults to “rising” to avoid a missing prior reference.

8. Exports:

A function that returns MACD, signal, smoothed histogram, the resolved lengths, and a text tag.

A function that returns the boolean rising state.

A function that returns a numeric one-or-zero series for direct plotting or downstream numeric logic.

HTF note: this is not a true higher-timeframe request. It does not fetch higher-timeframe candles. It approximates HTF feel by selecting different lengths on the current timeframe.

Parameter Guide

Source — Input price series used for EMA calculations — Default close — Trade-offs/Tips

Preset — Selects the hardcoded mapping family — Default preset A — Preset A is more reactive than preset B in typical use

Table Position — Anchor for an information table — Default top right — Present but not wired in the provided code (Unknown/Optional)

Table Size — Text size for the information table — Default normal — Present but not wired in the provided code (Unknown/Optional)

Dark Mode — Theme toggle for the table — Default enabled — Present but not wired in the provided code (Unknown/Optional)

Show Table — Visibility toggle for the table — Default enabled — Present but not wired in the provided code (Unknown/Optional)

Zero dead-band (epsilon) — Intended neutral band around zero for regime classification — Default zero — Present but not used in the provided code (Unknown/Optional)

Acceptance bars (n) — Intended debounce count for regime confirmation — Default three — Present but not used in the provided code (Unknown/Optional)

Smoothing length — Length controlling the histogram smoother’s responsiveness — Default nine — Smaller values react faster but can reintroduce flip noise

Reading & Interpretation